The Law of Anomalous Numbers, also known as Benford’s Law,

seeks to explain why the leading digits in any numerical

distribution skew low. In a uniform distribution, each number

(ignoring zero) has an 11.1% chance of being present. But that is

not the way it works out in real life, as the number one has up to

a 30% chance of being the leading digit in any arbitrary integer

base. The number two has an 18% chance of being the leading digit,

and so on. Thus, if the Law of Anomalous Numbers applied to IRS

guidance, the number of insurance tax releases in any given year

would be small. Lucky for us, though, in early 2021, the Internal

Revenue Service (“IRS”) and the Tax Court bucked

Benford’s Law and released a large number of insurance tax

items. The subject matter of the guidance spans a variety of

topics, including (i) the qualification of certain modified

co-insurance agreements as reinsurance, (ii) an analysis of certain

aspects of the base erosion anti-abuse tax (the “BEAT”)

for a domestic entity switching reinsurance counterparties, (iii)

whether a micro-captive arrangement constituted

“insurance” for US federal income tax purposes and (iv)

the taxation of certain annuity advisor fees under the terms of a

variable annuity contract.

I. PLR 202109005: Related-Party Risk Assumption Agreements

Qualify as Reinsurance

PLR 202109005 holds (but with scant discussion) that a

reinsurance contract of related-party risk (stemming from

diversified third-party risk) constitutes “insurance” for

US federal income tax purposes, even when the insured must step up

its premium payments to reimburse the insurer for sustained losses.

The amount of loss and premiums are not specified, however, making

it difficult to determine the actual amount of loss borne by the

risk-assuming party. It is also a straightforward application of

the position of the IRS as expressed in Revenue Ruling 2009-26: A

taxpayer is permitted to determine whether there has been risk

distribution and shifting on a look-through basis when the risk has

already been aggregated by an affiliate. The ruling helpfully holds

(but with scant discussion) that a reinsurance contract of

related-party risk (stemming from diversified third-party risk)

constitutes “insurance” for US federal income tax

purposes.

In the ruling, a non-US corporation regulated as an insurance

company (“Retrocessionare”) owned a domestic corporation

(“Parent”). Retrocessionare itself is owned by a non-US

publicly traded insurance holding company. Parent owns all of the

stock of a non-US reinsurance company, acting as reinsurer, that

elected to be treated as a domestic corporation under Code §

953(d) (“Reinsured”).

Reinsured is regulated as an insurance company in its

jurisdiction of formation. Reinsured entered into various

reinsurance agreements under which it assumed the risk under

deferred and immediate annuity contracts issued by, or in some

cases reinsured by, Reinsured’s affiliates. Reinsured then

insures against its risk with Retrocessionare through a renewable

modified co-insurance contract. (When a reinsurance company insures

itself, the transaction is referred to as “retrocession,”

and the party assuming the reinsurance risk is referred to as the

“retrocessionaire.”) The co-insurance arrangement was

subject to mandatory renewal if the Retrocessionaire’s payments

and payment obligations exceeded the premiums payable by the

Reinsured. The Reinsured could be required to make additional

payments to the Retrocessionaire under the co-insurance payments as

well, raising an issue as to whether the Retrocessionaire truly

bore risk. These payments likely would have been characterized as

additional premiums payable to the Retrocessionaire. The payments

under the co- insurance arrangement were determined by actuarial

analysis.

The arrangement between the parties that is the subject of the

ruling is set forth in Figure 1 below.

The parties sought a ruling that the co-insurance arrangements

would be treated as insurance for federal income tax purposes. Our

speculation is that Reinsured sought a ruling on this question due

to the uncertainty as to whether there was risk shifting in this

transaction due to the fact that premiums could be increased if the

Retrocessionaire experienced losses. If the transaction failed to

be treated as insurance, premiums paid to the Retrocessionaire

could have been subjected to a 30% withholding tax instead of the

much lighter excise tax on insurance premiums.

The IRS began its analysis with an overview of the guidance on

what constitutes “insurance.” As is oft- repeated by the

IRS and the courts, the US tax law does not provide a definition of

“insurance,” but the Supreme Court has provided four key

features for distinguishing insurance from other arrangements:

- Traditional insurance. An insurance

arrangement is “insurance” in its commonly accepted

sense, generally depending on whether the entity is organized,

operated, and regulated as insurance company, has adequate

capitalization, and receives reasonable arm’s- length premiums,

among other factors;1 - Insurance risk. The arrangement is over an

“insurance risk”; - Risk shifting. The insurance risk is shifted

from one party to the other in the arrangement; and - Risk distribution. The party insures the risk

pools and distributes that risk.2

The Code specifies that “insurance” includes the

issuance of annuity contracts.3 PLR 202109005 concludes

that the Contract constitutes reinsurance. Thus, the first two

tests were clearly met.

The IRS has previously offered guidance on risk distribution for

aggregated risks in Revenue Ruling 2009-26.4 There,

through a single reinsurance contract, a corporation reinsured the

risk to another insurance company of 90% of all losses on insurance

contracts with 10,000 unrelated policyholders.

The Revenue Ruling holds that despite the reinsurer entering

into only one contract, because the risks of each original

policyholder were distributed among the pool of policyholders, the

reinsurer’s risk was distributed through the single contract.

But this look-through rule requires that there be risk

diversification in the original transaction. In Revenue Ruling

2005-40, the IRS held that a purported insurance arrangement

involving an issuer who contracts with only one policyholder does

not qualify as insurance contracts because issuer did not

distribute the risk.5 PLR 202109005 does not specify the

number of annuity policies underlying the Contract, it appears to

be substantial.

II. PLR 202109001: Substituting Related-Party Reinsurers Does

Not Trigger BEAT Payment

The BEAT functions as an alternative minimum tax in that

specified taxpayers must make a parallel calculation to their

regular tax liability and, to the extent such amount is greater

than the taxpayer’s regular tax liability, the BEAT imposes tax

equal to the excess of the BEAT liability over the regular tax

liability. At the heart of the BEAT calculation is the concept of a

base erosion payment and, for each type of base erosion payment,

the corresponding base erosion tax benefit. These concepts

determine whether specified taxpayers are subject to BEAT, and if

so, the amount of the BEAT liability. There are four types of base

erosion payments enumerated in the statute.6 One type of

base erosion payment is an amount paid or accrued by the taxpayer

to a foreign person for reinsurance payments taken into account

under Code § 803(a)(1)(B) or Code § 832(b)(4)(A) (in

which case the base erosion tax benefits are the reduction to gross

income and the deduction provided for in such sections).

The BEAT applies only to taxpayers that are corporations (other

than regulated investment companies, real estate investment trusts,

or S corporations) that have average annual gross receipts of at

least $500 million over a three-year period and, have a base

erosion percentage of at least 3% (or, if they are a domestic bank,

the base erosion percentage during the taxable year is at least

2%).

The BEAT liability, if any, is calculated by adding back to

taxable income a taxpayer’s base erosion tax benefits, plus the

base erosion percentage of the taxpayer’s post-2017 net

operating loss deductions for the taxable year. The result,

referred to as “modified taxable income,” is then

multiplied by an applicable tax rate. For tax years 2019 through

2025, the applicable tax rate is 10% and after 2025, the rate is

12.5%. (These rates are increased by 1% for US banks.) As stated

above, if the BEAT exceeds the regular tax liability reduced by

certain tax credits, the taxpayer will owe the BEAT amount.

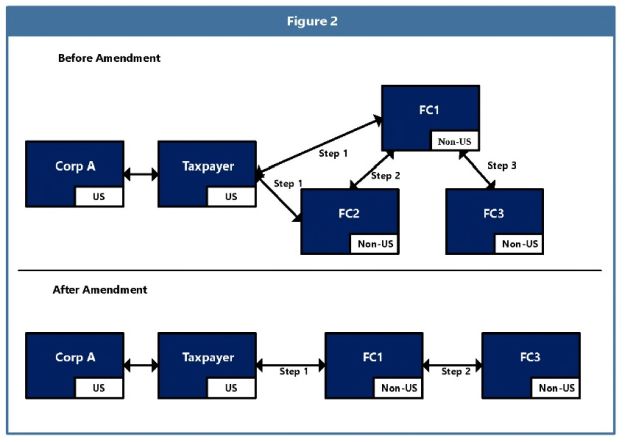

In PLR 202109001, the taxpayer, a domestic corporation that was

part of an affiliated group filing a consolidated federal income

tax return, reinsured risk under certain insurance policies that it

had written with another member of the affiliated group (“Corp

A”). The taxpayer ceded a portion of this risk to its indirect

non-US owner, a non-US corporation (“FC1”). The taxpayer

also ceded a portion of this risk to an indirect non-US subsidiary

of FC1 (“FC2”), which ceded the risk to FC1.

FC1 also ceded a portion of the Corp A risks to another non-US

subsidiary (“FC3”). To reduce operational complexity and

administrative burden, the parties desired to remove intervening

step 1 involved FC2 in transferring the Corp A risks from Taxpayer

to FC1. Diagrammatically, the arrangements were as follows:

The issue appeared to be whether the substitution of FC1 for FC2

triggered a sale or exchange of the ceding agreement by the

Taxpayer. See Rev. Rul. 90-109, 1990-2 CB 191 (change of

insured triggered gain or loss inherent in an insurance contract);

Estate of McKelvey v. Comm’r, 906 F3d 26 (2d Cir.

2018) (extension of variable prepaid forward contract triggered a

sale or exchange of the contract). The IRS noted that the

assumption by FC1 is an assumption reinsurance transaction within

the meaning of Treasury Regulation §

1.809-5(a)(7)(ii).7 Case law states that an assumption

reinsurance transaction is treated as a sale by the ceding company

to the reinsuring company.8 If this treatment governed

the consequences for the taxpayer, and the taxpayer had a loss on

such sale, the loss could have been treated as a base erosion

payment.

PLR 202109001, citing Revenue Ruling 82-122, 1982-1 CB 80,

concludes that the substitution of FC1 for FC2 resulted in the sale

of the contract. The IRS highlights that the premiums to be paid by

the Taxpayer were unaltered by changing the counterparty. Because

of this, the IRS concluded that any amount paid on the assumption

should be between FC1 and FC2, not a premium or other deductible

payment made by Taxpayer to a foreign affiliate that could give

rise to a base erosion payment for purposes of the Taxpayer’s

BEAT calculation. In other words, from the perspective of the

Taxpayer, the IRS essentially treated the substitution of

reinsurers as a modification that was not material, given that the

payments to be made by the Taxpayer did not change as a result of

the substitution. The analysis of the IRS appears to dovetail with

the rule in Treasury Regulation § 1.1001-3(e)(4)(iv). Under

that regulation, a change in credit enhancement on a debt

instrument triggers a sale or exchange only if there is a change in

payment expectations. The authors also note that Treasury

Regulation § 1.1001-4, relating the substitutions of

counterparties on derivatives, reaches the same conclusion for the

non-transferring party on those contracts when such contracts are

transferred between dealers or clearinghouses.

III. Caylor Land & Development, Inc. v.

Comm’r, TC Mem. 2021-30 (March 10, 2021)

“Micro-captive” insurance transactions can offer

substantial tax benefits. On one hand, the payment of the premiums

can be deductible to the insured. On the other hand, if the net

written premiums received by the insurance company do not exceed

$2.2 million, the insurance company does not pay tax on the premium

income.9 The IRS has taken a dim view of small insurance

company transactions in which the insurance company is related to

the companies from which it has assumed risk. In Notice 2016-66,

modified by Notice 2017-8, 2017-3 IRB 423, the IRS identified

certain micro-captive insurance transactions as “transactions

of interest.”10 The IRS has been on a tear

litigating, and winning, decisions against micro- captive

transactions. See Avrahami v. Comm’r, 149 T.C. No. 7

(2017); Reserve Mechanical Corp. v. Comm’r, TC Mem.

2018-86; Syzygy Insurance Co. v. Comm’r, TC Mem.

2019-34. On April 9, 2021, the IRS announced that it had formed 12

audit teams dedicated solely to challenging micro-captive

transactions.11 Previously, it had offered a limited

time settlement to taxpayers who participated in these

transactions.12

The IRS’s string of victories against micro-captive insurers

continued into early 2021 with strong decision in the Tax Court in

Caylor Land & Development, Inc. v.

Commissioner.13

In Caylor, a family owned a variety of entities in the

business of commercial construction. The Caylors historically

purchased third-party insurance (and continued to do so during the

years at issue) but decided to also form a captive insurance

company in Anguilla with an election for the company to be a Code

§ 953(d) company. The premiums deducted by the Caylor entities

and paid to the captive were $1.2 million in each year covered by

the decision (the then maximum amount permissible for the captive

to pay no tax on premiums received). Although twelve Caylor

entities paid premiums to the captive, the Tax Court observed that

one Caylor entity, Caylor Land, was the revenue generator for the

family of affiliates, and all funds to pay the insurance premiums

ultimately flowed from Caylor Land. The premiums in each year were

paid before contracts for each year outlining the insurance

policies were drafted. During the three year period of coverage,

the captive paid four claims that amounted to $43,000. The captive

paid the claims without receiving requested information about the

claims, an action which the court noted is not standard practice

for an insurance company. Across the entities, the insurance

covered 34 different exposures.

The Tax Court begins its analysis with the four Le

Gierse factors discussed above, concluding that the

arrangement did not satisfy the requirement that the captive

distribute its risk and the requirement that the arrangement was

insurance in its commonly accepted sense. On risk distribution, the

Tax Court examined whether the captive distributed the risk among a

sufficient number of unrelated risks for the law of large numbers

to predict expected losses (as in other Tax Court precedent). In

finding the captive did not, the Tax Court first emphasized in

cases where a captive arrangement was respected, captives insured

risks in the thousands.14 This leaves a grey area

between the thirty-four independent exposures assumed by the

captive in Caylor and the thousands accepted as satisfying

the law of large numbers in the Tax Court’s other precedents.

Second, the Tax Court reasoned that risk distribution is better

supported where the risks are more independent than under the facts

of Caylor, where all risks insured by the captive were

related to the real estate business in a single geographic

area.

Although in Revenue Ruling 2005-40, the IRS interpreted risk

distribution to require both many insureds and many risks, the Tax

Court has been less clear. Both Rent-A-Center and at least

one other case presented instances of many risks but only one or

two insureds. In Avrahami, the court said without any

analysis (or mention of Rent-A-Center) that three insureds

are insufficient. The court in Caylor refrains from

clearly adopting the IRS’s requirement of many insureds but

satisfies itself by saying the law of large numbers means more than

the 30 or so risks involved in that caser. We are still waiting for

the Tax Court to agree or disagree with whether the IRS’s

position in Revenue Ruling 2005-40 that 10,000 risks from only one

customer does not accomplish risk distribution.

In finding that the captive arrangement in Caylor was

not insurance in its commonly accepted sense, the Tax Court held

that (a) the captive did not act as an insurance company and the

Caylor entities did not act as insureds, since the parameters of a

policy were not established for a taxable year until after premiums

had been paid and claims were paid on the policies without the

captive receiving requested information about the claims, and (b)

the premiums paid to the captive were far in excess of any expected

loss and were calculated by including an adjustment mechanism meant

to reach the then-$1.2 million cap under Code § 831(b).

Since the Tax Court found that the captive arrangement was not

insurance in the commonly accepted sense and that it lacked risk

distribution, the Court held that the arrangement between the

Caylor entities and the captive was not insurance.

Caylor highlights some bad facts to watch out for when

structuring a captive arrangement meant to be characterized as

insurance.

IV. Annuity Adviser Fees Paid Net Not Taxable to the Annuity

Owner

One of the tax benefits of whole life insurance and variable

annuities (together, variable contracts) is that the investment

component of the contracts can be taxed in the same manner as death

benefits and periodic payments. In other words, variable contracts

offer investment returns on these products that are taxed much more

favorably than if the insured or annuitant held the same

investments outside of an insurance product. In order for the

investment component of a variable contract to receive this

favorable tax regime, the insurance contract must meet certain

diversification and investor control requirements. The

diversification requirements are spelled out in Treasury Regulation

§ 1.817-5. The IRS has spelled out the investor control

requirements, however, through a series of rulings and other

authorities. See Webber v. Commissioner, 144 TC 324 (2015)

(IRS position on investor control adopted by Tax Court).

Traditionally, the IRS interpreted the investor control

requirement in a rigid manner. In Rev. Rul. 77-85, 1977-1 C.B. 12,

the IRS concluded that an individual purchaser of a variable

annuity contract who retained “significant incidents of

ownership” over the assets held in the custodial account was

treated as the owner of those assets for federal income tax

purposes. In Rev. Rul. 80- 274, 1980-2 C.B. 27, the IRS applied

Rev. Rul. 77-85 to conclude that if a purchaser of an annuity

contract could select and control the certificates of deposit

supporting the contract, then the purchaser was considered the

owner of the certificates of deposit for federal income tax

purposes. Similarly, in Rev. Rul. 81-225, 1981-2 C.B. 12, which was

clarified and amplified by Rev. Rul. 2003-92, 2003-2 C.B. 350, the

IRS concluded that investments in mutual fund shares that funded

annuity contracts were considered to be sub-accounts. Each

sub-account invested in interests in a partnership. The IRS held

that in situations in which the sub-accounts held interests in

partnerships available for purchase other than by purchasers of

annuity or variable contracts from an insurance company, the

contract-holder was the owner of the interests in the partnerships

held by the sub-accounts for federal income tax purposes.

In recent years, the IRS has relented on this rigid approach and

has been issuing private letter rulings to taxpayers that variable

contract holders would not be treated as the owner of the

underlying investments where the underlying investments can be

chosen by a licensed investment advisor chosen by the insured. The

rulings even permit the investment advisor to be affiliated with

the issuer of the variable contract. The issuing insurer will pay

fees to the adviser for investment advice that the adviser provides

to the variable contract owner with respect to the variable

contract. The variable contracts offered numerous investment

options for the insured or annuitant where the advisor, in

consultation with the insured, allocated the contract corpus among

these investment choices. The IRS recently issued a number of

private rulings holding that these advisory schemes did not violate

the investor control requirement. See e.g., PLR 202104001,

PLR 20205004, PLR 20205006, PLR 202024008, and more.

In March and April 2021, the IRS released several private letter

rulings holding that annuity advisor fees under a variable annuity

contract which were deducted from the cash value of the annuity

contract for investment advisory services rendered to the insured

under variable contracts did not constitute deemed distributions to

the contract owner.15 As part of the contract, the

Adviser provided ongoing investment advice to contract owners in

exchange for a fee. Rather than charge the owner a fee directly or

from any distribution from the variable contract to the owner, the

Adviser was paid by the insurer from the cash value of the annuity

contract.

Economically, it could have been viewed as though the owner was

distributed cash which was then paid to the Adviser for the

adviser’s services under the contract.

The IRS held the amounts withdrawn as advisory fees should not

be treated as an “amount received” by the beneficial

owner of the contract. The ruling concludes that the beneficial

owner should not treat the advisory fees as an amount received from

the annuity contract. Taking an “entity-level” approach

to the fees, the rulings find that the fees are an expense of the

investment contract, not the beneficial owner, because (a) the

contract was designed to depend on the ongoing investment advice,

(b) the fees will only be used to pay for advisory services under

the contract and will not be consideration for any other service,

and (c) the fees were reasonable at 1.5%. The structure of this

transaction effectively allows the investor to deduct the cost of

the investment manager’s fees despite the 2% floor and the

suspension of Code § 67 deductions subject to the 2% floor

through 2025.

Although the PLRs are noticeably silent on the investor control

requirement, they assume without discussion that the arrangements

will not violate such requirement. The advisor works directly with

the variable contract owner to determine the allocation among

investment strategies available within the segregated accounts held

by the insurance company that are dedicated to the variable

contract and are paid by the insurer. Under prior IRS guidance,

variable contract owners would have been concerned that this type

of arrangement would have caused the contract owner to have control

over the assets held by the insurer. The fact that the IRS is now

issuing rulings on this structure is likely to further enhance the

market for variable contracts.

Footnotes

* Brennan and Mark are both tax lawyers

with the New York office of Mayer Brown. Mark and Brennan each work

with insurance tax issues on a regular basis. Mark and Brennan

express their thanks to George “Buz” Craven, Mayer

Brown’s insurance tax guru, for his thoughts and comments on an

earlier version of this Legal Update. Mistakes and omissions,

however, remain the sole responsibility of the authors. The views

expressed herein are solely those of the authors and should not be

imputed to Mayer Brown.

1. See, e.g.,

Avrahami v. Commissioner, 149 T.C. 144 (2017).

2. Helvering v. E. Le Gierse,

312 U.S. 351 (1941)

3. See Code section 816(a),

where a life insurance company is defined as an insurance company

which is engaged in the business of issuing life insurance and

annuity contracts with corresponding reserves in excess of 50% of

its total reserves.

4. Rev. Rul. 2009-26, 2009-39 IRB 366

(2009).

5. Rev. Rul. 2005-40, 2005-2 CB 4

(2005).

6. The term “base erosion tax

benefit” also includes amounts paid to related foreign persons

to acquire depreciable property (in which case the base erosion tax

benefit is the depreciation deductions), amounts paid to related

foreign persons for reinsurance payments taken into account under

Code § 803(a)(1)(B) or Code § 832(b)(4)(A) (in which case

the base erosion tax benefits are the reduction to gross income and

the deduction provided for in such sections), and amounts paid or

accrued by a taxpayer that result in reductions in gross receipts

if the payment is to a related “surrogate foreign

corporation” or to a foreign person in the same expanded

affiliated group as the surrogate foreign corporation (in which

case the base erosion tax benefit is the reduction in gross

receipts).

7. Under that regulation, assumption

reinsurance as an arrangement whereby another person (the

reinsurer) becomes solely liable to the policyholders on the

contracts transferred by the taxpayer (not including indemnity

reinsurance or reinsurance ceded).

8. Beneficial Life Ins. v.

Commissioner, 79 T.C. 627 (1982), nonacq. on other

grounds, 1982-2 C.B. 1.

9. Code section 831(b)(1).

10. Notice 2016-66, 2016-47 IRC 745

(2016). A transaction of interest is a “reportable

transaction,” which generally requires all participants to the

transaction (and their material advisers) to file forms with the

IRS describing the transaction. A failure to properly report a

transaction of interest results in penalties of up to $10,000 for

natural persons and $50,000 for all other taxpayers. See

Code section 6707A(b)(2)(B).

11. See IRS News Release,

IRS urges participants of abusive micro-captive insurance

transactions arrangements to exit from arrangements (IR-

2021-82) (Apr. 9, 2021).

12. See Clock Ticking for

Micro-Captives Considering IRS Settlement Offer (2) (Bloomberg News

Sep. 17, 2019).

13. Caylor Land & Development,

Inc. et. al. v. Commissioner, T.C.M. 2021- 30 (March 10,

2021)

14. See Harper Grp. v.

Commissioner, 96 T.C. 45 (1991), aff’d 979 F. 2d

1341 (9th Cir. 1992) (captive insured 7,500 customers covering more

than 30,000 different shipments and 6,722 special cargo policies);

Rent-A-Center, Inc. v. Commissioner, 142 T.C. 1 (2014)

(captive insured three types of risks covering 14,000 employees,

7,000 vehicles, and 2,600 stores); and R.V.I. Guar Co. v.

Commissioner, 145 T.C. 209 (2015) (captive insured one type of

risk through 951 policies covering 714 insured parties with more

than 754,000 passenger vehicles, 2,00 individual real-estate

property, and 1.3 million commercial-equipment assets).

15. See, e.g., PLR 202109002,

PLR 202109003, PLR 202114005, and PLR 202114006.

Visit us at

mayerbrown.com

Mayer Brown is a global legal services provider

comprising legal practices that are separate entities (the

“Mayer Brown Practices”). The Mayer Brown Practices are:

Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited

liability partnerships established in Illinois USA; Mayer Brown

International LLP, a limited liability partnership incorporated in

England and Wales (authorized and regulated by the Solicitors

Regulation Authority and registered in England and Wales number OC

303359); Mayer Brown, a SELAS established in France; Mayer Brown

JSM, a Hong Kong partnership and its associated entities in Asia;

and Tauil & Chequer Advogados, a Brazilian law partnership with

which Mayer Brown is associated. “Mayer Brown” and the

Mayer Brown logo are the trademarks of the Mayer Brown Practices in

their respective jurisdictions.

© Copyright 2020. The Mayer Brown Practices. All rights

reserved.

This

Mayer Brown article provides information and comments on legal

issues and developments of interest. The foregoing is not a

comprehensive treatment of the subject matter covered and is not

intended to provide legal advice. Readers should seek specific

legal advice before taking any action with respect to the matters

discussed herein.